Non Performing Assets (NPAs) have become a significant concern for the banking sector, impacting economic stability and growth. This is of particular concern for a growing economy like India. This article aims to study in detail the concept of Non Performing Assets, its meaning, classification, reasons for increasing NPAs, steps taken to curb its rise and other related concepts.

What is Non Performing Assets (NPAs)?

A non performing assets refer to loans or advances, the principal or interest payment for which remained overdue for a period of 90 days.

Classification of Non Performing Assets

Based on the period of interest payment overdue, Non Performing Assets are classified into the following three categories.

Substandard Assets

Assets that have been classified as Non Performing Assets for a duration of 12 months or less are referred to as Substandard Assets.

Doubtful Assets

If the asset remains in the substandard category for a period of 12 months, it is categorized as Doubtful Asset.

Loss Assets

Those assets which have become uncollectible and are no longer continue as a bankable asset.

Reasons for Increasing Non Performing Assets

- Over-optimism of Banking Sector: Bank did not show much accountability and diligence when the economy was growing and infrastructure improved during 2006-08.

- Slow Growth: The financial crisis of 2008 led to slower economic growth which in turn affected the profits of the companies and reduced their ability to pay back the loans on time.

- External Factors: To counter the aftermath of the financial crisis and declining growth, major central banks globally adopted the easy money policy which also resulted in easy liquidity in emerging markets such as India.

- This phenomenon pushed up asset prices and led to inflation and also posed threat of stagflation.

- Regulatory and Policy Risks: A volatile regulatory framework in the country in the past few years has led to stress in certain industries.

- For example, Mining ban in certain southern Indian states caused significant financial and operating stress in companies engaged therein, which had a cascading effect on overall investments in the Indian economy.

- Industry Specific Risks: There are industry-specific reasons that cause a rise in the level of Non Performing Assets in India.

- For example, higher Non Performing Assets in aviation sector could be attributed to high cost of aviation turbine fuel. For Indian airlines, turbine fuels constitute 45% of total operating costs, as compared to the global average of 30%.

- Poor Credit Appraisal System: The credit appraisal by the banks before giving loans remains of low quality.

- Diversion of Loans: The poor end-use monitoring system of the Banks has led to diversion of funds by the companies for other wasteful purposes.

- Wilful Defaulters: A lack of proper mechanisms to deal with them means that there has been an increase in the number of wilful defaulters.

- Wilful Defaulters refer to those loanees who fail to repay back the loans despite of being capable of doing so.

- Red-Tapism: Delays in government approvals led to increase in the number of stalled projects.

- Lack of Policy Foresight: Legal provisions to deal with Non Performing Assets such as Insolvency and Bankruptcy Code (IBC) and SARFAESI Act have been formulated only recently.

- Frauds: The system has failed to bring any high-profile fraudsters to justice. It was only after the NPA crisis that the RBI established a fraud monitoring cell to facilitate the early reporting of fraud cases to investigative agencies.

- Ineffective Recovery Tribunal: There has been undue delay in the resolution of cases before the debt recovery tribunals leading to higher Non Performing Assets.

- Political Interference in working of PSBs: The Non Performing Assets are mainly concentrated in the Public Sector Banks which could be linked to their poor governance, political interference and lack of independent decision making body.

- Priority Sector Lending: The lending by the Banks to priority sectors such as Agriculture and MSMEs has also contributed to Non Performing Assets.

- Credit Culture: The frequent announcement of farm loan waivers by the Central has affected the credit culture in India.

- Absence of Integrated Database on Credit Information: Presently, the credit related information is captured by multiple agencies without proper coordination.

- The RBI’s proposal of creating Public Credit Registry faces legal challenges.

Impact of Rising Non Performing Assets

Rising Non Performing Assets has negative impact the overall growth of the economy as can be seen below.

- Profitability: On an average, banks are providing around 25% to 30% additional provision on incremental Non Performing Assets which has direct bearing on the banks’ profitability.

- Asset (Credit) Contraction: The increased Non Performing Assets has reduced the banks’ ability to lend more and thus lesser interest income.

- It contracts the money stock which may lead to economic slowdown.

- Liability Management: High Non Performing Assets may make Banks lower the interest rates on deposits on one hand and levy higher interest rates on advances.

- This may become hurdle in smooth financial intermediation process and hampers banks’ business as well as economic growth.

- Capital Adequacy: According to Basel norms, banks must maintain sufficient capital for their risk-weighted assets.

- An increase in the level of Non Performing Assets adds to risk weighted assets which requires the banks to shore up their capital base further.

- In case of PSBs, it may put additional burden on the Government for recapitalisation of PSBs.

- Shareholders’ Confidence: The rise in Non Performing Assets is likely to negatively affect the bank’s business and profitability. As a result, shareholders may not receive a market return on their capital, and their investment value could erode.

- Public Confidence: The credibility of the banking system is significantly impacted by high levels of NPAs, as it undermines the general public’s confidence in the system’s stability and reliability.

Steps Taken to Curb NPAs

- Debt Recovery Tribunal (DRT): It was set up in 2013 to reduce the time required for settling cases.

- It is governed by Recovery of Debt due to Banks and Financial Institutions Act, 1993.

- Credit Information Bureau: It was set up in 2000 to prevent NPAs by sharing of information on wilful defaulters.

- Asset Reconstruction Companies (ARCs): ARCs have been set up to fasten the recovery of value from stressed loans, bypassing courts.

- Reconstruction of Financial Assets and Enforcement of Security Interests (SARFAESI) Act, 2002: This act provides the legal framework for securitization activities in India.

- It grants banks and financial institutions the authority to seize immovable property that has been pledged to recover debts, without needing to go through the Debt Recovery Tribunal (DRT).

- Corporate Debt Restructuring: It was implemented in 2005 to alleviate the debt burden on companies by extending the repayment period as well as reducing interest rates.

- 5:25 Rule: Introduced in 2014, it is also known as Flexible Restructuring of Long-Term Project Loans for Infrastructure and Core Industries.

- Joint Lenders Forum (JLF): Established in 2014, it was designed to prevent scenarios where a loan from one bank is used to repay loans from other banks.

- Mission Indradhanush: It was launched in 2015 as a comprehensive 7-pronged reforms to improve the functioning of the Public Sector Banks.

- The reforms under Mission Indradhanush include: Appointments, Bank Board Bureau, Capitalisation, De-stressing, Empowerment, Framework for Accountability, and Governance Reforms.

- Strategic Debt Restructuring (SDR): This scheme was launched in 2015 under which if the corporates, who have taken loans from banks, are unable to repay, the banks can convert part or complete loans into equity shares.

- Asset Quality Review (AQR): Initiated in 2015 as a preventive measure, it involves the early identification of assets that might become stressed in the future.

- Insolvency and Bankruptcy Code (IBC): It was enacted in 2016 and lays down clear-cut and faster insolvency proceedings to help creditors, including banks, recover dues and prevent bad loans.

Read our detailed article on Insolvency and Bankruptcy Code (IBC).

- Bad Bank: Bad Bank is a specialised Asset Reconstruction Company (ARC) that purchases NPAs from banks and restructures them.

Read our detailed article on Bad Bank.

Conclusion

Non Performing Assets pose a significant challenge to the banking sector and the economy. While various measures have been taken to address the issue, it requires continuous efforts to prevent a recurrence and maintain financial stability. A robust credit culture, effective risk management, and strong governance are essential for mitigating NPA risks.

Special Mention Account (SMA)

- It is an account showing early signs of stress that may lead to the borrower defaulting on timely debt servicing, even though it has not yet been classified as an Non Performing Asset according to current RBI guidelines.

- SMAs show symptoms of bad asset quality and have potential to become an NPA/Stressed Asset.

| SMA Sub-categories | Basis for classification – Principal or interest payment overdue between |

|---|---|

| SMA-0 | 1-30 days |

| SMA-1 | 31-60 days |

| SMA-2 | 61-90 days |

Twin Balance Sheet Problem (TBS)

Twin Balance Sheet Problem (TBS) refers to a two-fold problem for Indian economy which include:

- Overleveraged Companies: Reasons such as stalled projects and poor demand, etc lead to inability of companies to pay off their debt. This leads to debt accumulation and rising NPAs.

- Bad-Loan-Encumbered Banks: As companies fail to pay back principal or interest, banks are also in trouble. Rising Non Performing Assets leads to reduced incomes from assets (RoA) which necessitates increased provisioning and declining profits making banks risk averse and reluctant to lend.

| 40% of corporate debt is owed by companies who are not earning enough to pay back their interest payments. |

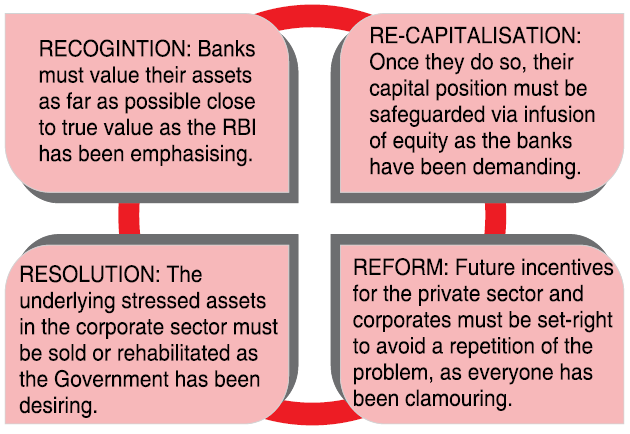

Four R Resolution Approach

- The Economic Survey 2015-16 has suggested ‘Four R (4R) Resolution Approach’ to comprehensively resolve the issues of rising Non Performing Assets and Twin Balance Sheet problem.

- The 4 Rs of the approach include:

Frequently Asked Question

What is the full form of NPA?

NPA full form is Non Performing Asset.