Blockchain technology is a decentralized, secure, and transparent digital ledger system that records transactions across multiple computers. It ensures data integrity using cryptography, enabling trust without intermediaries. Widely applied in cryptocurrencies like Bitcoin, it also powers smart contracts, supply chain management, and more, revolutionizing industries with efficiency and immutability.

What is Blockchain Technology?

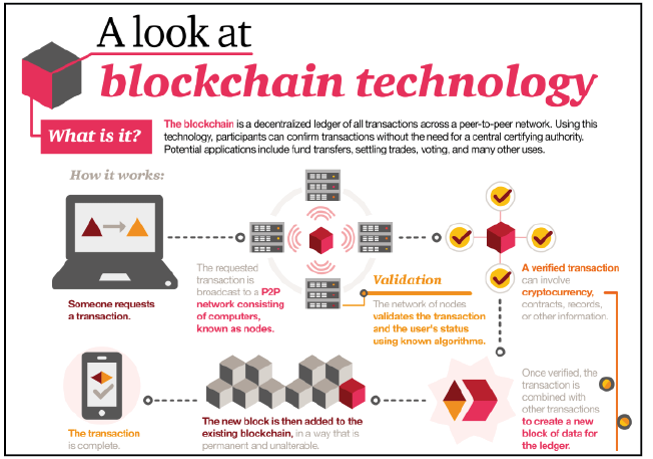

- Blockchain technology is most simply defined as a decentralized, distributed ledger that records the provenance of a digital asset. By inherent design, the data on a blockchain is unable to be modified, which makes it a legitimate disruptor for industries like payments, cybersecurity and healthcare, banking etc.

Features

- Every user can access the entire blockchain, and every transfer of funds from one account to another is recorded in a secure and verifiable form by using mathematical techniques borrowed from cryptography.

- With copies of the blockchain scattered all over the planet, it is considered to be effectively tamper-proof.

- Law enforcement and international currency controls are the challenges.

- Like the Internet, the blockchain technology is an open, global infrastructure upon which other technologies and applications can be built.

- Like the Internet, it allows people to bypass traditional intermediaries in their dealings with each other, thereby lowering or even eliminating transaction costs.

- It is estimated that by 2022, blockchain technology could save banks more than $20 billion annually in costs.

- By using the blockchain, individuals can exchange money or purchase insurance securely without a bank account, even across national borders i.e. a feature that could be transformative for the two billion people in the world currently underserved by financial institutions.

- Blockchain technology lets strangers record simple, enforceable contracts without a lawyer.

- It makes it possible to sell real estate, event tickets, stocks, and almost any other kind of property or right without a broker.

- The technology doesn’t make theft impossible, just harder. It has the potential to enhance privacy, security and freedom of conveyance of data (problems that continue to plague Internet commerce).

- Because blockchain transactions are recorded using public and private keys—long strings of characters that are unreadable by humans. People can choose to remain anonymous while enabling third parties to verify that they shook, digitally, on an agreement.

Applications of Blockchain Technology

Blockchain technology has numerous applications across various industries due to its secure, transparent, and decentralized nature. Key applications include:

- Cryptocurrencies: Enabling secure digital currencies like Bitcoin and Ethereum.

- Smart Contracts: Automating agreements without intermediaries.

- Supply Chain Management: Enhancing transparency and traceability.

- Healthcare: Securing patient records and improving data sharing.

- Banking and Finance: Streamlining cross-border payments and fraud detection.

- Voting Systems: Ensuring transparent and tamper-proof elections.

- Identity Management: Offering secure, verifiable digital identities.

- Real Estate: Simplifying property transfers with tokenized assets.

- Gaming: Enabling ownership of in-game assets and NFTs.

- Energy Sector: Supporting peer-to-peer energy trading.

Blockchain’s versatility is driving innovation across many fields.

India’s Stand on Blockchain Technology

India has recognized the transformative potential of blockchain technology and is actively exploring its applications across sectors. The government’s stance on blockchain can be summarized as follows:

- Proactive Adoption:

- India is embracing blockchain for public services like land records, supply chain management, and digital identity.

- Several state governments, including Andhra Pradesh and Telangana, have launched pilot projects utilizing blockchain.

- Policy Development:

- The Reserve Bank of India (RBI) and other regulatory bodies are studying blockchain for financial systems, including central bank digital currency (CBDC) initiatives.

- The government released a draft framework for blockchain adoption in 2021 under the Ministry of Electronics and Information Technology (MeitY).

- Promotion of Research:

- India is investing in blockchain research through initiatives like the National Blockchain Framework and partnerships with tech companies.

- The Indian Institute of Technology (IITs) and other institutions are establishing blockchain innovation hubs.

- Cryptocurrency Regulation:

- While cautious about cryptocurrencies due to risks like money laundering and fraud, India differentiates between blockchain as a technology and its application in cryptocurrencies.

- The government proposed a Digital Rupee and is working on cryptocurrency legislation.

India’s approach emphasizes leveraging blockchain for economic growth, governance, and transparency, while addressing regulatory concerns with balanced policies.

Benefits Of Blockchain Technology

Blockchain technology offers several benefits that make it transformative for businesses and industries:

- Enhanced Security

- Data is encrypted and stored across decentralized networks, reducing vulnerability to hacks and unauthorized access.

- Immutability ensures records cannot be altered once validated.

- Transparency

- Transactions are recorded on a shared ledger accessible to authorized participants, promoting trust and accountability.

- Decentralization

- Removes reliance on a central authority, reducing risks of single points of failure and enhancing system resilience.

- Cost Efficiency

- Reduces intermediaries in processes like payments, supply chain management, and document verification, lowering costs.

- Traceability

- Enables real-time tracking of assets in industries like supply chain, agriculture, and healthcare, ensuring authenticity and reducing fraud.

- Speed and Efficiency

- Automates processes using smart contracts, reducing manual interventions and speeding up transactions.

- Improved Data Integrity

- Immutable records ensure data accuracy and reliability, crucial for sectors like healthcare, finance, and logistics.

- Empowerment of Users

- Provides individuals control over their data through secure identity management and self-sovereign digital identities.

- Innovation in Finance

- Facilitates decentralized finance (DeFi), enabling peer-to-peer lending, borrowing, and trading without intermediaries.

- Global Accessibility

- Offers equal opportunities for participation in global systems like cryptocurrencies, especially in underserved regions.

Blockchain’s benefits are driving its adoption across industries, promoting efficiency, security, and trust.

Disadvantages of Blockchain Technology

Despite its transformative potential, blockchain technology has several disadvantages and challenges:

- High Energy Consumption

- Certain blockchain systems, like Bitcoin, rely on energy-intensive proof-of-work (PoW) consensus mechanisms, impacting environmental sustainability.

- Scalability Issues

- Blockchains often struggle to handle a large number of transactions simultaneously, leading to slower processing times and higher fees.

- Complexity and Learning Curve

- The technology is still relatively complex, requiring significant technical expertise for implementation and maintenance.

- Regulatory Uncertainty

- Many countries lack clear regulations around blockchain and cryptocurrencies, creating legal ambiguities for businesses and users.

- High Initial Costs

- Implementing blockchain solutions can be expensive due to the need for infrastructure, skilled professionals, and system customization.

- Lack of Interoperability

- Many blockchains operate in isolation, making it challenging to integrate or share data across different platforms.

- Data Immutability Challenges

- While immutability ensures data integrity, it can be problematic if errors or fraudulent data are entered, as they cannot be corrected.

- Storage and Network Limitations

- The growing size of blockchain ledgers requires significant storage space and bandwidth, which can limit participation for smaller nodes.

- Potential for Misuse

- Decentralization and anonymity can facilitate illicit activities, such as money laundering and cybercrime.

- Dependency on Internet Access

- Blockchain systems require constant internet connectivity, limiting their functionality in regions with poor infrastructure.

While blockchain offers numerous advantages, addressing these disadvantages is crucial for its widespread adoption and success.

Way Forward

Blockchain technology involves enhancing scalability, energy efficiency, and interoperability through advanced consensus mechanisms and protocols. Clear regulations, skilled workforce development, and industry collaboration are essential for fostering innovation.

Promoting research, public-private partnerships, and integration into critical sectors like healthcare, finance, and governance can unlock blockchain’s full potential, driving transparency, security, and economic growth globally.

Conclusion

Blockchain technology is a transformative innovation offering unparalleled security, transparency, and efficiency across industries. Despite challenges like scalability and regulatory concerns, its potential to revolutionize finance, supply chains, healthcare, and governance is immense. With ongoing advancements, blockchain is poised to become a cornerstone of the digital economy and modern innovation.

GS - 3