Syllabus: GS3/Energy

Context

- Recently, the Ministry of Statistics and Programme Implementation (MoSPI) has unveiled its annual publication, ‘Energy Statistics India 2025’, through the National Statistics Office (NSO).

India’s Energy Scenario in 2025

- Total Energy Supply and Demand:

- Supply: Approximately 1,800 Million Tonnes of Oil Equivalent (MToE), reflecting an annual increase of 4.5% compared to 2024.

- Demand: It is driven primarily by industrial growth (40%), transportation (25%), and residential consumption (20%).

- Energy Mix (Sources and Shares):

- Coal: 48%

- Oil: 28%

- Natural Gas: 8%

- Renewables (Solar, Wind, Hydro, Biomass): 12%

- Nuclear: 4%

- Fossil Fuel Reserves and Production (Total coal reserves: 320 billion tonnes):

- Coal Reserves and Production: The distribution of coal reserves in India is concentrated in a few states like Odisha (25.47%), Jharkhand (23.58%), Chhattisgarh (21.23%), West Bengal (8.72%) and Madhya Pradesh (8.43%).

- These states account for approximately 85% of the total coal reserves in India.

- Total estimated reserves of lignite as on 01-04-2024 stood at 47.30 billion tonnes. The highest reserves of lignite are located in the state of Tamil Nadu (79%).

- Annual coal production: 950 million tonnes, meeting 85% of domestic demand.

- India remains the second-largest coal producer globally, after China.

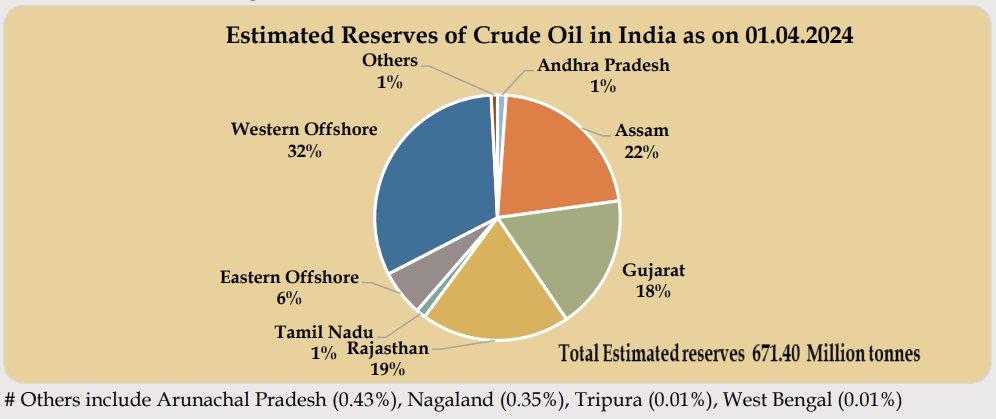

- Crude Oil: Geographically, the maximum crude oil reserves in India are concentrated in the Western Offshore region (32% of the total crude oil reserves). It is followed by the Assam region (22% of the country’s crude oil reserves).

- Coal Reserves and Production: The distribution of coal reserves in India is concentrated in a few states like Odisha (25.47%), Jharkhand (23.58%), Chhattisgarh (21.23%), West Bengal (8.72%) and Madhya Pradesh (8.43%).

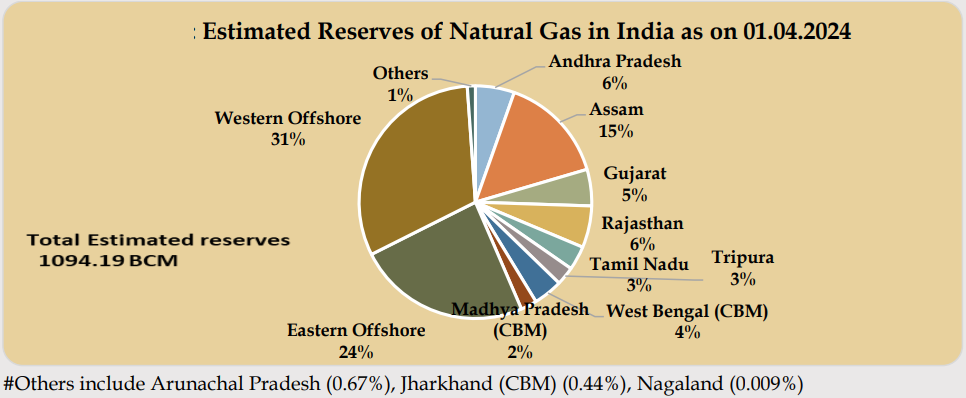

- Natural Gas Reserves: Largest reserves of natural gas in India are located in the Western Offshore region (approximately 31% of the total natural gas reserves). It is followed by the Eastern Offshore (approx 24% of the reserves).

Renewable Energy Growth

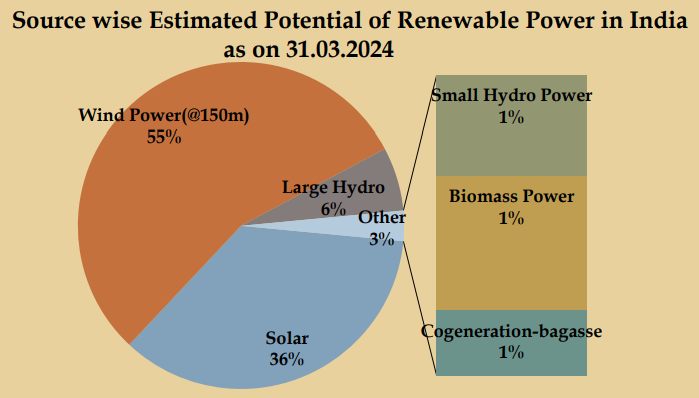

- Potentials: Wind Power dominates share (around 55%), followed by Solar Energy and Large Hydro.

- Geographical Distribution of Renewable Energy Potential: More than half of the potential for generation of renewable energy has been concentrated within the four States of India viz. Rajasthan (20.3%), Maharashtra (11.8%), Gujarat (10.5%) and Karnataka (9.8%).

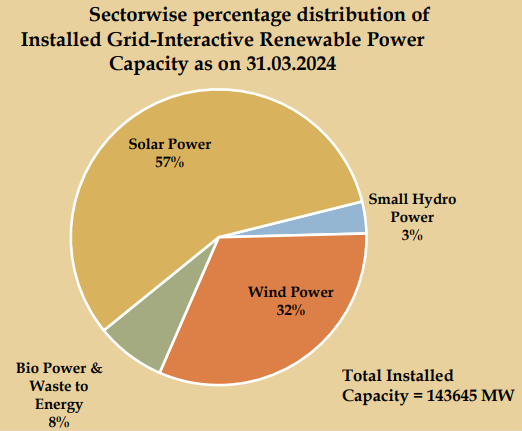

- Solar and Wind Power Expansion: The National Solar Mission and Wind Energy Development Programme have played a crucial role in achieving these milestones:

- Solar Power Capacity: 175 GW (up from 150 GW in 2024)

- Wind Power Capacity: 50 GW (up from 45 GW in 2024)

- Hydro and Biomass Energy:

- Hydropower: 52 GW, providing 12% of total electricity generation.

- Biomass and Waste-to-Energy: 15 GW, contributing to sustainable energy practices in rural areas.

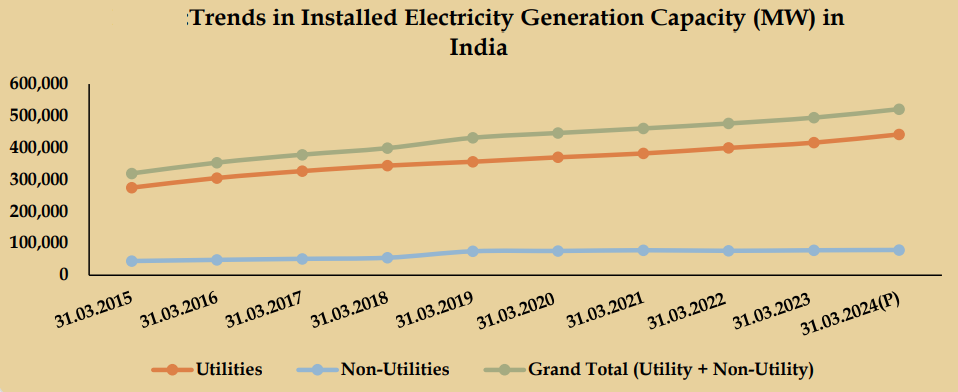

- Electricity Generation and Consumption Trends:

- Installed Capacity and Generation: India’s total installed power generation capacity stands at 450 GW, an increase from 420 GW in 2024.

- Total electricity generation: 1,700 TWh (terawatt-hours).

- Per capita electricity consumption: 1,500 kWh per year, reflecting economic growth and urbanization.

- Distribution and Transmission:

- Transmission losses have reduced to around 17% during FY 2023-24 (23% during FY 2014-15) due to Smart Grid Initiatives.

Energy Efficiency and Sustainability Measures

- Government Policies and Initiatives:

- National Hydrogen Mission: Promoting Green Hydrogen production for industrial use.

- Perform, Achieve, and Trade (PAT) Scheme: Encouraging industries to adopt energy-efficient technologies.

- Faster Adoption of Electric Vehicles (FAME-III): Boosting EV sales and charging infrastructure.

- Carbon Emissions and Climate Targets:

- India’s carbon emissions in 2025 are projected at 2.9 billion tonnes CO₂, a 4% decline due to increased renewable energy usage.

- Commitment to net-zero emissions by 2070 remains a long-term goal.

Future Outlook

- Future Energy Projections (2026-2030):

- Renewable energy share is expected to reach 25% by 2030.

- Energy demand will continue growing at 5% annually, driven by economic expansion.

Challenges Ahead

- Dependence on Fossil Fuels: India still relies heavily on coal and imported crude oil.

- Energy Security Risks: Geopolitical uncertainties affect oil and gas imports.

- Infrastructure Bottlenecks: Need for grid modernization and storage solutions for renewables.

Previous article

India, US To Jointly Design, Manufacture Nuclear Reactors In India

Next article

Why Are Tensions High in the Arctic?