Syllabus: GS3/ Economy

In News

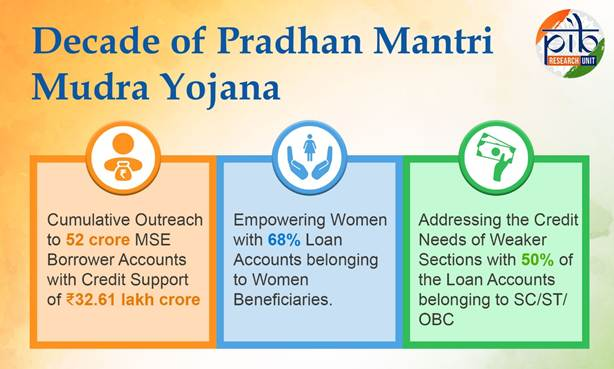

- On 8 April 2025, India marked 10 years of the Pradhan Mantri MUDRA Yojana (PMMY).

About the Scheme

- Launched: April 2015

- Objective: To provide collateral-free institutional credit to non-corporate, non-farm micro and small enterprises.

- Tagline: Funding the Unfunded

- Implementation: Through MUDRA (Micro Units Development and Refinance Agency).

- Target: Small businesses in manufacturing, trading, processing, and services—a major employment segment after agriculture.

- Collateral-free credit up to ₹20 lakh is provided by Member Lending Institutions (MLIs) i.e. Scheduled Commercial Banks (SCBs), Regional Rural Banks (RRBs), Non-Banking Financial Companies (NBFCs) and Micro Finance Institutions (MFIs).

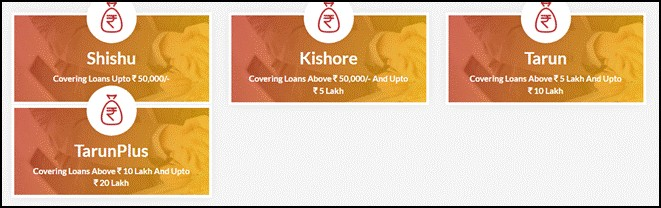

- Loan Categories under PMMY:

- Achievements (As of FY25)

- Loans sanctioned: Over 52 crore

- Loan value: ₹32.61 lakh crore

Need For Funding the Unfunded (MSME)

- Micro enterprises constitute a major economic segment in India and provide large employment after agriculture. This segment includes micro units engaged in manufacturing, processing, trading and services sector.

- It provides employment to nearly 10 crore people. Many of these units are proprietary/ single ownership or Own Account enterprises and many a time referred to as the Non-Corporate Small Business sector.

International Recognition

- IMF has praised PMMY across multiple reports:

- 2017: Helped women-led businesses access credit.

- 2019: Recognized its role in refinancing MSMEs.

- 2023: Highlighted over 2.8 million women-owned MSMEs.

- 2024: Acknowledged PMMY as key to formalisation and self-employment.

Significance

| Women Empowerment | 1. 68% of beneficiaries are women 2. Per woman disbursement CAGR: 13% 3. Enhanced economic independence and labour force participation |

| Marginalised Communities | 1. 50% of Mudra accounts are SC/ST/OBCs 2. 11% Mudra accounts belong to minority communities 3. Bridges financial exclusion and promotes inclusive growth |

| Boost to MSME Credit | 1. MSME credit rose from ₹8.51 lakh crore (FY14) to ₹27.25 lakh crore (FY24) 2. Projected to cross ₹30 lakh crore in FY25 3. MSME share in total bank credit increased from 15.8% to ~20% |

| Job Creation | 1. Supports self-employment and entrepreneurship 2. Generates jobs in tier-2/3 cities and rural areas |

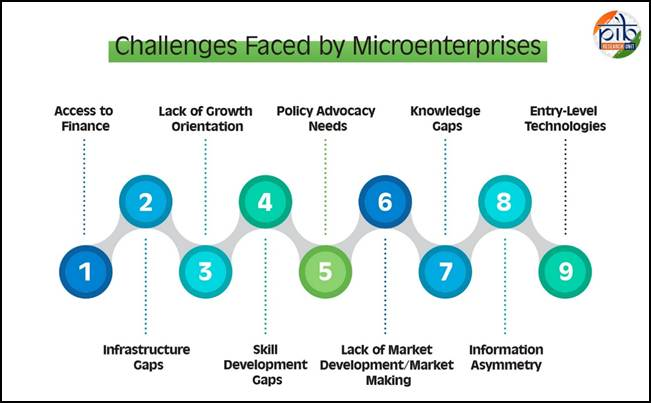

Challenges

- Risk of NPAs (Non-Performing Assets) in some sectors.

- Need for better credit appraisal and training of borrowers.

- Require complementary ecosystems (e.g., market access, digital literacy).

Conclusion

- In ten years, Pradhan Mantri Mudra Yojana has consistently demonstrated the power of financial inclusion and the strength of grassroots innovation.

Source: PIB

Previous article

New Policy on Foreign Funds