Syllabus: GS3/ Economy

Context

- India’s microfinance sector is witnessing a rise in delinquencies, even as the overall banking sector records a 12-year low in non-performing assets (NPAs).

What is Microfinance?

- Microfinance refers to the provision of small loans and financial services to low-income groups who lack access to traditional banking channels.

- Microfinance institutions (MFIs) play a pivotal role in financial inclusion by offering credit to underserved populations, primarily for entrepreneurial activities and income generation. Types of MFIs are;

- Non-Banking Financial Companies – Microfinance Institutions (NBFC-MFIs).

- Non-Governmental Organizations (NGOs): It operates as non-profit organizations.

- Cooperatives: They are Member-owned institutions providing microfinance services.

- Commercial Banks and Small Finance Banks (SFBs): Provide microfinance as part of their priority sector lending.

Current Scenerio

- Rising Delinquencies:

- Microfinance loans to low-income groups have shown a sharp increase in Portfolio at Risk (PAR) (overdue loans of 31-180 days).

- Geographic Impact: Bihar, Tamil Nadu, Uttar Pradesh, and Odisha account for 62% of new late payments.

- Delinquencies are increasing across all loan categories, with Small Finance Banks (SFBs) being most affected.

- Market Share and Growth:

- NBFCs and banks together hold 71.3% of the total microloan portfolio.

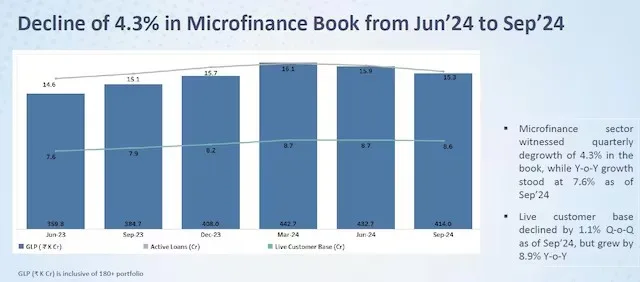

- Despite a 7.6% year-on-year growth in the loan book and an 8.9% rise in the live customer base, there was a quarterly decline of 4.3% in the loan book and 1.1% in the customer base.

Reasons for Rising Delinquencies

- Borrower Overleveraging: Increased borrowing from both MFI and non-MFI sources has resulted in excessive debt burdens among borrowers.

- Instances of Frauds: Cases of misrepresentation and fraudulent practices have led to heightened operational risks.

- Economic Distress: External economic shocks and income uncertainties have impacted repayment capacities.

- Operational Challenges: High staff attrition and lack of proper borrower assessment mechanisms.

Impact of Rising Delinquencies

- Financial Strain on MFIs: Increased credit costs reduce profitability for MFIs, affecting their financial stability.

- Reduced Lending Capacity: Higher NPAs limit the ability to extend fresh credit to borrowers, hampering financial inclusion.

- Borrower Distress: Overleveraged borrowers face economic hardships and risk exclusion from financial systems.

- Sector-Wide Confidence Issues: Rising defaults can diminish investor and lender confidence in the microfinance ecosystem.

Way Ahead

- Strengthening Credit Assessment: Implementing better risk profiling and borrower assessment mechanisms.

- Financial Literacy Initiatives: Enhancing borrower awareness regarding credit management.

- Stricter Regulatory Oversight: Strengthening supervision to prevent fraud and malpractices.

- Operational Strengthening: Reducing staff attrition through better training and incentives.

- Debt Consolidation Measures: Offering structured repayment plans for overleveraged borrowers.

Concluding remarks

- To ensure the long-term health of the microfinance sector, a balanced approach involving stronger credit discipline, financial education, and regulatory vigilance is essential.

- Addressing structural vulnerabilities and promoting responsible lending practices will be crucial for sustaining financial inclusion in India.

Sources: IE

Previous article

Data Localization in India

Next article

India’s Need for Authentic and Impactful Research