Syllabus: GS3/ Economy

Context

- The RBI’s restrictions on New India Co-operative Bank highlight ongoing vulnerabilities within the urban cooperative banking sector.

What are Cooperative Banks?

- Cooperative Banks refer to those financial institutions under the Banking System in India that operate on the principles of cooperation and mutual benefit for their members.

- They belong to their members who are both the owners and customers of the bank.

- They operate on the principle of “one person, one vote” in decision-making. Along with lending, these banks also accept deposits.

Regulation of Cooperative Banks in India

- These banks in India, broadly, come under the dual control of:

- Reserve Bank of India: Under the Banking Regulation Act, 1949, and the Banking Laws (Application to Co-operative Societies) Act, 1965, the RBI is responsible for regulating banking aspects of these banks, such as capital adequacy, risk control, and lending norms.

- Registrar of Co-operative Societies (RCS) of respective State or Central Government: They are responsible for regulation of management-related aspects of these banks, such as incorporation, registration, management, audit, supersession of board of directors, and liquidation.

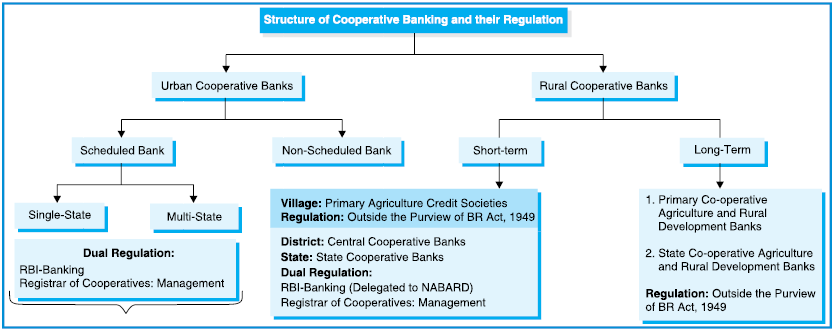

Structure of Cooperative Banks in India

- These banks, under the Banking System in India, are primarily categorized into – Rural Cooperative Banks (RCBS), and Urban Cooperative Banks (UCBS).

- They are further sub-categorised as shown below:

Urban Cooperative Banks (UCBs)

- They operate in urban and semi-urban areas and mainly lend to small borrowers and businesses.

- Based on their regulation regime, they are categorized into two types – Scheduled Banks and Non-Scheduled Banks.

Issues in Urban Cooperative Banks (UCBs)

- Cooperative Banks are facing financial vulnerabilities such as low capitalization, high levels of NPAs, and low Capital Adequacy Ratio (CAR).

- A large number of big Cooperative banks have failed due to financial scams. Ex-Punjab and Maharashtra Cooperative (PMC) bank, Guru Raghavendra Cooperative Bank and Maharashtra State Cooperative (MSC) Bank have failed due to financial frauds.

Reasons for Recurring Issues in the UCBs

- Regulatory Arbitrage: Cooperative banks escape stringent RBI scrutiny compared to commercial banks.

- Political Interference: Many cooperative banks are influenced by local politicians, leading to poor governance.

- Limited Technological Adoption: Many UCBs lack robust digital infrastructure, making them susceptible to operational inefficiencies and fraud.

- Weak Risk Management Practices: Inadequate internal controls result in unchecked lending, increasing bad loans.

Measures to Strengthen the Cooperative Banking Sector

- Capital Adequacy Norms: Cooperative banks should maintain higher capital buffers to withstand financial shocks.

- Technology Upgradation: Adoption of digital banking, fraud detection mechanisms, and improved cyber security measures.

- Consolidation of Weak Banks: Merging smaller, financially weak cooperative banks with larger, stable ones will enhance their resilience.

- Governance Framework: Stricter norms for board composition, qualifications of directors, and independent audits must be enforced.

Source: BS

Next article

Government to Lease Out 10 Airports via PPP Model