Syllabus :GS 3/Economy

In News

- India’s investment ecosystem and External Commercial Borrowings (ECBs) have witnessed significant developments over the past few years.

About

- The recent report by the State Bank of India (SBI) has highlighted trends in investment announcements, private sector’s contribution, and role of ECBs in corporate financing.

- Household Net Financial Savings (HNFS) in India improved to 5.3% of GDP in FY24 from 5.0% in FY23.

- Investment as a share of GDP has improved in recent years, led by both government and private sector contributions.

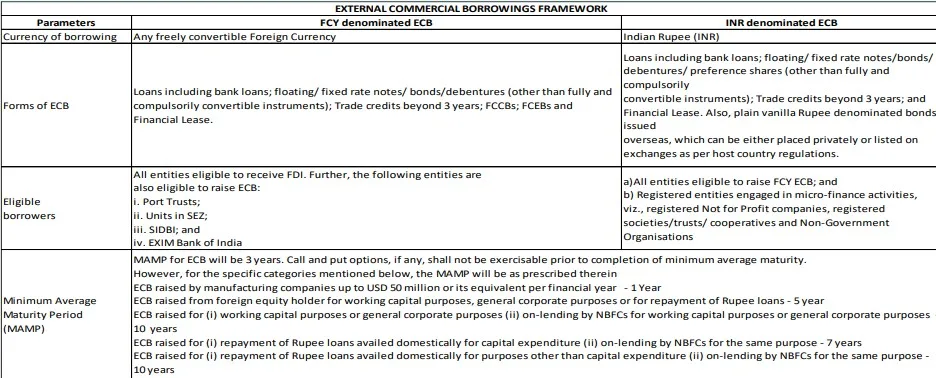

External Commercial Borrowings

- External Commercial Borrowings are commercial loans raised by eligible resident entities from recognised non-resident entities.

- These borrowings have to conform to parameters such as minimum maturity, permitted and non-permitted end-uses, maximum all-in-cost ceiling, etc.

Framework and Guidelines

| Data Analysis of SBI’s recent report – External Commercial Borrowings (ECBs) (as of September 2024) have emerged as a key source of funding for Indian corporates, enabling capital expansion and modernization. 1. The total outstanding ECBs stood at $190.4 billion as of September 2024. 2. Of this, the non-Rupee and non-FDI components accounted for approximately $154.9 billion. 3. The private sector held 63% ($97.58 billion), while the public sector accounted for 37% ($55.5 billion). 4. Hedging remains a critical aspect, with private companies hedging approximately 74% of the total hedged corpus. 5. ECBs in FY25 (Up to November 2024) : The ECB pipeline remains strong, reflecting sustained demand for overseas funding. |

The Need for ECBs in India

- Capital Shortage: Domestic financial markets may not meet the needs of large corporations.

- Lower Interest Rates: ECBs often offer lower rates than domestic loans, reducing the cost of capital.

- Filling Infrastructure Gap: India’s infrastructure sector requires significant investments.

- Diversification of Funding: Access to global markets reduces reliance on domestic banks.

- Support for Export-Oriented Sectors: Helps businesses modernize and stay competitive internationally.

- Boost to Corporate Growth: Enables expansion, technology upgrades, and enhanced market position.

Limitations and Risks of ECBs

- Currency Risk: Exchange rate fluctuations can increase repayment costs if the domestic currency depreciates.

- Interest Rate Risk: Variable interest rates tied to global benchmarks (e.g., LIBOR) can make loans expensive as rates rise.

- Repayment Risk: Short maturities may lead to refinancing challenges, especially if funds are not readily available.

- Regulatory Constraints: Strict RBI regulations on borrowing limits, end-use, and compliance can limit flexibility.

- Macroeconomic Risks: Excessive reliance on ECBs can increase national external debt and strain foreign exchange reserves.

Conclusion and Way Forward

- External Commercial Borrowings have become an essential tool for Indian companies looking to access global capital and finance large-scale projects.

- ECBs offer significant potential to fuel India’s growth, particularly in sectors like infrastructure, technology, and exports.

- However, companies must carefully evaluate their financial position and risk appetite before opting for external borrowings to ensure they are leveraging this financial instrument effectively and sustainably.

Source :PIB

Previous article

India – Oman FTA Agreement Talks

Next article

News In Short 28-1-2025