Syllabus: GS2/Governance

Context

- The Pradhan Mantri Jan Dhan Yojana (PMJDY), launched in 2014 under the Ministry of Finance has completed a decade of successful implementation.

About

- PMJDY being the largest financial inclusion initiative to provide support to the marginalised and economically backward sections through its financial inclusion interventions.

- PMJDY provides one basic bank account for every unbanked adult.

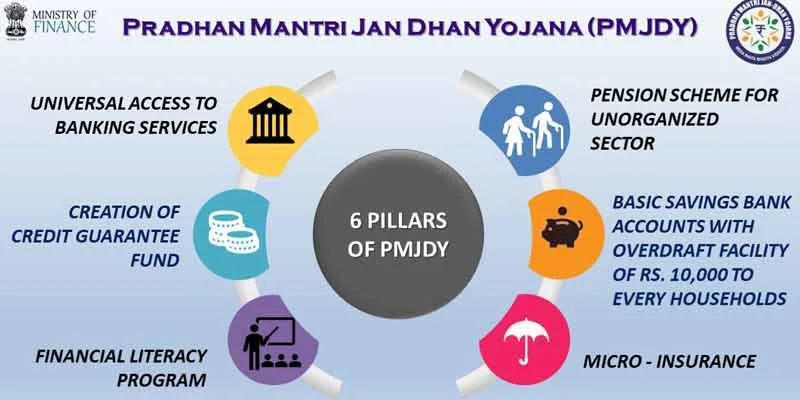

Key Features of the Jan Dhan Yojana

- Under the PMJDY, individuals can open a basic savings bank deposit (BSBD) account at any bank branch or through a Business Correspondent (‘Bank Mitra’).

- Key benefits of the scheme include:

- No requirement to maintain a minimum balance in PMJDY accounts;

- Interest earned on deposits in PMJDY accounts;

- Provision of a RuPay Debit card to account holders;

- Accident insurance cover of Rs 100,000 (increased to Rs 200,000 for new accounts opened after August 28, 2018) with the RuPay card;

- Overdraft facility of up to Rs 10,000 for eligible account holders;

- Eligibility for Direct Benefit Transfer (DBT), Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY), Pradhan Mantri Suraksha Bima Yojana (PMSBY), Atal Pension Yojana (APY), and Micro Units Development and Refinance Agency Bank (MUDRA) scheme.

Significance

- The PMJDY serves as a platform for hassle-free subsidies/payments made by the government to the intended beneficiary without any middlemen, seamless transactions, and savings accumulation.

- They have been crucial in providing life and accident insurance to millions of unorganized sector workers through Jan Suraksha schemes (micro insurance schemes).

Successful Implementation of the Scheme

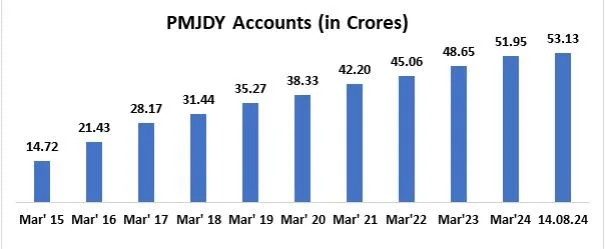

- The success of the initiative is reflected in 53 crore people having been brought into the formal banking system through the opening of Jan Dhan Accounts.

- These bank accounts have garnered a deposit balance of Rs. 2.3 lakh crore, and resulted in the issuance of over 36 crore free-of-cost RuPay cards, which also provide for a ₹2 lakh accident insurance cover.

- 67% of the accounts have been opened in rural or semi-urban areas, and 55% of accounts have been opened by women.

Conclusion

- PMJDY’s success highlights its mission-mode approach, regulatory support, public-private partnerships, and the importance of digital public infrastructure like Aadhaar for biometric identification.

- Account holders can now show saving patterns, which makes them eligible for loans from banks and financial institutions.

- PMJDY being the world’s largest financial inclusion scheme, with its transformative power and its digital innovations have revolutionised financial inclusion in India.

Source: PIB

Previous article

Centers Promoting Classical Languages Demanding Autonomy